Market Amid New Tariffs – Keeping Perspective

Trump’s Sweeping New Tariffs: What’s in Them?

President Trump jolted markets this week by unveiling sweeping new tariffs on U.S. imports. In a surprise “Liberation Day” proclamation, the White House announced a 10% across-the-board tariff on all goods imported into the U.S., effective April 5. On top of that, even higher levies target countries deemed “bad actors” on trade. For example, imports from Japan now face a 24% duty and those from the European Union 20%, starting April 9. China was hit hardest – subject to an additional 34% tariff (on top of existing duties), bringing the base tariff rate on Chinese goods to a staggering 54%. These tariffs span virtually all categories, from toothbrushes to televisions, amounting to the largest U.S. import tax hike in decades (the average U.S. tariff rate will leap to the highest in over a century.

Certain industries are singled out as well. Foreign automobiles and parts now face a 25% import tariff, a long-threatened measure that officially took effect at 12:01 AM on April 3. This auto tariff is expected to add thousands of dollars to new vehicle prices, weighing on auto sales. (Auto parts will see equivalent tariffs by next month, compounding the impact on carmakers.) Notably, Canada and Mexico were excluded from the new “reciprocal” global tariffs regime. However, imports from those NAFTA partners aren’t completely off the hook – separate plans for 25% tariffs on most Mexican and Canadian imports remain on the table (with exemptions for autos and various other goods). In short, no major U.S. trading partner is untouched by this broad tariff campaign. Key sectors from technology and electronics to retail, apparel, and machinery are bracing for higher import costs.

Even though energy products were exempted from tariffs, the breadth of affected goods is immense. Which countries are hit? Virtually all of them. The tariff schedule is meant to mirror (“reciprocate”) the import duties those nations impose on the U.S. Over 180 countries – including close allies – are subject to the 10% base tariff. Around 60 countries with whom the U.S. has large trade imbalances or longstanding disputes face the steeper rates. China’s rate is highest (reflecting issues like market access and the fentanyl dispute). Other major economies like the EU, Japan, South Korea, India, and Vietnam are also in the “worst offenders” group with double-digit tariffs. What goods are targeted? Essentially everything: the tariffs cover a vast range of products Americans buy – electronics, clothing, appliances, furniture, automobiles, and more. As one report noted, consumers could see prices jump on items “from toothbrushes to televisions”. These import taxes act much like a sales tax on consumer goods, and this package has been called the biggest tax hike on U.S. consumers since the 1940s. While some U.S. manufacturers may benefit from less foreign competition, businesses that rely on global supply chains are facing tough decisions.

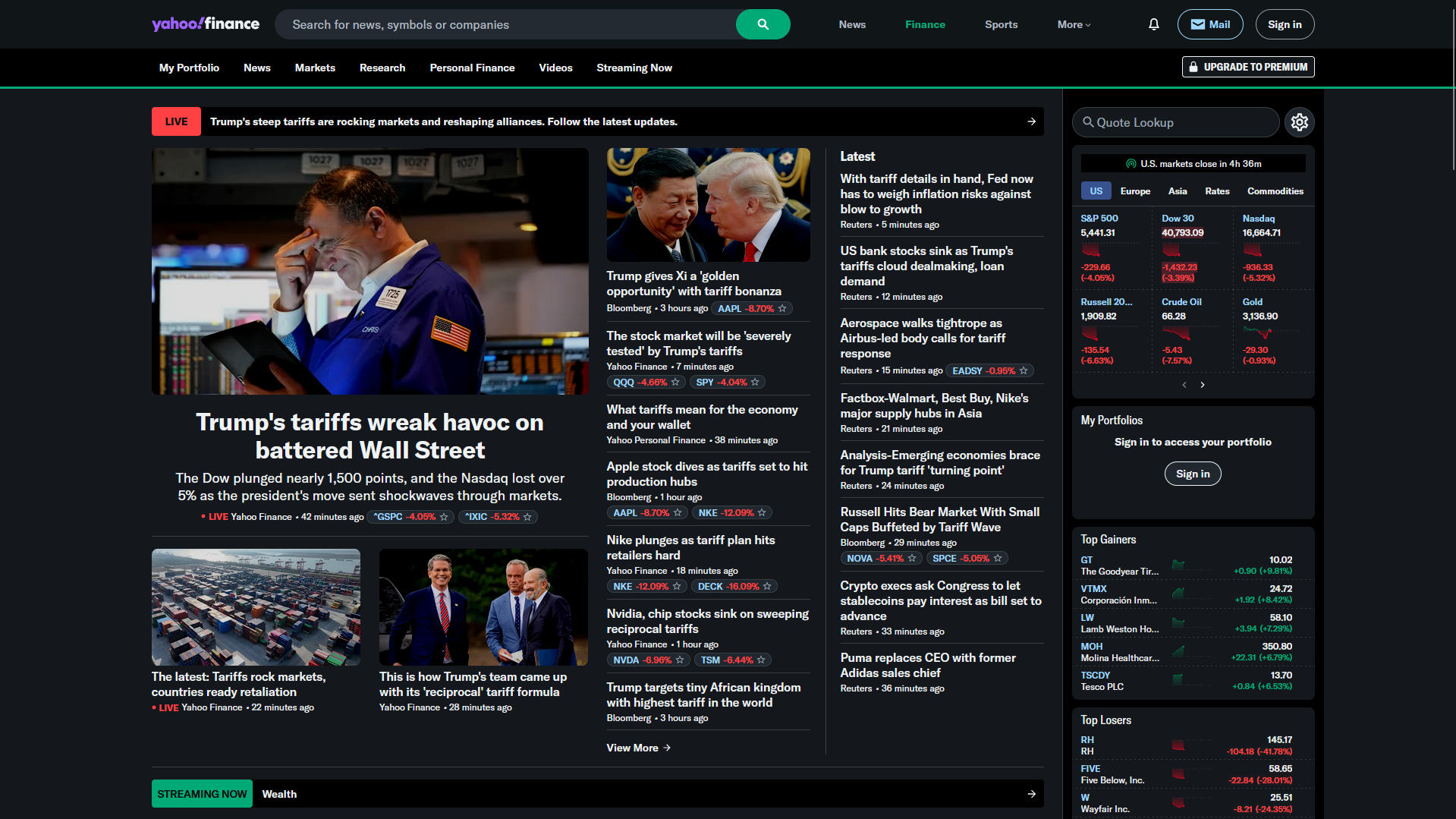

Yahoo Finance front page reacts to market volatility following Trump’s “Liberation” tariff announcement.

Trump’s Objectives: Why the U.S. is Pursuing This Tariff Policy

President Trump’s new tariff initiative is being framed as a bold step toward creating a more balanced and fair global trade environment. At the heart of the policy is the idea of “reciprocal tariffs”—ensuring that if other countries impose high trade barriers on American goods, the U.S. responds in kind. As shown in the graphics below, many trading partners have historically taxed U.S. exports at significantly higher rates than we’ve applied to theirs. This new approach seeks to level the playing field, promote American manufacturing, and encourage more equitable treatment of U.S. businesses abroad. While markets are reacting to the short-term uncertainty, the White House’s long-term vision is one of greater self-reliance, stronger domestic production, and improved negotiating leverage. If successful, these policies could pave the way for more balanced trade agreements and reduced dependence on global supply chains.

Markets React: Shockwaves Across Stocks, Bonds, and Currencies

The immediate market reaction was swift and negative worldwide. U.S. stocks sold off sharply on the tariff news, with major indexes enduring their worst drop in over a year. The Dow Jones Industrial Average plunged over 1,000 points (a ~3–4% decline), while the S&P 500 fell about 3.7% and the tech-heavy Nasdaq Composite slumped nearly 5%. By the time of writing this blog, the Dow was down roughly 1,300 points (about –3.4%) and the Nasdaq –4.6%. In percentage terms, these losses echo the kind of single-day drops seen during past trade war scares. Investors dumped riskier assets across the board – everything from industrial blue-chips to high-flying tech names sank. Market leadership like Apple and Amazon each fell in high-single digits, and the S&P 500’s broad decline officially pushed it into a “growth scare” correction territory.

The sell-off was global. European and Asian equity markets were not spared from the tariff shock. In Europe, export-focused sectors like autos and luxury goods were hit hard, despite Europe’s slightly lower 20% tariff rate. Germany’s DAX and France’s CAC 40 indexes slid in sympathy with Wall Street, as investors assessed the impact on European manufacturers. Chinese stocks tumbled overnight, and the Chinese yuan weakened to multi-month lows after Trump’s announcement, reflecting fears of diminished export prospects. In fact, China’s markets had an outsized reaction – the Shanghai and Shenzhen indexes fell sharply, and the yuan briefly breached the psychologically important level of 7.5 to the dollar (its biggest drop in years), underscoring concern about China’s growth outlook under a 54% U.S. tariff. Other Asian markets like Japan’s Nikkei and South Korea’s KOSPI also closed down ~2–3%. Global investors flocked to safe-havens, driving up bond prices and defensive assets.

In the currency markets, the U.S. dollar oddly fell on the news – a sign that investors see these tariffs as a negative for U.S. growth. The dollar sank over 2% against safe-haven currencies like the Japanese yen, Swiss franc, and even the euro. In fact, the dollar index slipped to its lowest level of the year as forex traders anticipated that trade disruptions could slow the flow of international capital into the U.S.. Typically one might expect the dollar to rise in a risk-off move, but this time concern about U.S.-specific fallout took precedence, weakening the greenback. Meanwhile, U.S. Treasury yields plunged as investors sought the safety of government bonds. The benchmark 10-year Treasury yield fell sharply, at one point nearing the 4.0% threshold from above. (Recall that falling yields mean rising bond prices.) This robust bond rally was a classic flight-to-quality response, reflecting worries that the tariffs could tip the economy toward slower growth or even recession. Credit markets showed signs of stress as well – yields on riskier corporate bonds ticked up and credit spreads widened modestly on the tariff headlines, indicating a higher perceived risk of defaults if corporate profits get squeezed.

Commodity markets added to the volatile mix. Oil prices slumped over 7% on Thursday, with Brent crude falling to just under $70 a barrel. Traders feared the trade war could sap global energy demand, and news that OPEC+ plans to boost output only added to the downward pressure on oil prices. Even gold, which had been on a strong run to record highs, saw some profit-taking – gold prices dipped nearly 2% as some investors sold to cover losses elsewhere. However, traditional safe havens like U.S. Treasuries and the Japanese yen clearly outperformed, fulfilling their role as shock absorbers in a turbulent market.

In summary, equity and credit markets worldwide echoed a classic “risk-off” reaction: stocks down, dollar down, yields down, and volatility up. The speed and magnitude of the decline underscore how blindsided Wall Street was by the scope of the tariff announcement. One moment the S&P 500 was hovering near all-time highs; the next, it was down almost 5% in a day. Still, it’s worth noting that trading remained orderly (no flash crashes or liquidity freezes reported), but still closed at session lows. Volatility spiked, but there were also buyers cautiously stepping in at the lows, suggesting that many investors view this shock as a short-term disruption rather than a permanent blow to the market’s longer-term trajectory.

Wall Street Journal highlights domestic equity market dislocation as reaction to Trump’s tariff announcement on April 2, 2025.

Historical Parallels: From Smoot-Hawley to the 2018 Trade War

Tariffs and trade wars have rattled markets before. History offers valuable context to help investors make sense of the current volatility. Perhaps the most infamous episode was the Smoot-Hawley Tariff Act of 1930, a sweeping protectionist law often blamed for exacerbating the Great Depression. Smoot-Hawley raised U.S. import duties by an average of ~20% – similarly aimed at protecting domestic industries – but it backfired disastrously (What Is the Smoot-Hawley Tariff Act? History, Effect, and Reaction). U.S. trading partners retaliated with tariffs of their own, global trade collapsed, and economic pain deepened worldwide. Economists widely agree that Smoot-Hawley worsened the severity of the Great Depression by choking off international trade. As global trade volumes plummeted, businesses and farmers lost export markets and millions of jobs were lost, creating a vicious cycle of decline. The U.S. stock market, already reeling from the 1929 crash, reacted negatively to Smoot-Hawley’s passage – it “coincided with the start of the Great Depression,” according to historians (Smoot-Hawley Tariff Act | History, Effects, & Facts | Britannica). In short, broad tariffs have a dark track record: the Smoot-Hawley Act triggered the “mother of all trade wars,” with over 35 countries raising tariffs in response, and ushered in a period where global trade shrank dramatically . That precedent is a big reason why markets are so sensitive to any whiff of protectionism.

More recently, we have the example of the 2018–2019 U.S.–China trade war. During President Trump’s first term, the U.S. and China exchanged several rounds of tariffs. That period provides a useful roadmap for how markets might behave now. In 2018, as tariffs on Chinese goods were first announced and implemented, stock markets went on a roller coaster ride. Each new tariff tweet or breakdown in negotiations tended to send stocks tumbling, only for optimism about resumed talks or temporary truces to spark rebounds. Indeed, volatility spiked as markets reacted to each twist in trade policy. For example, when talks broke down and new tariffs hit in mid-2019, the S&P 500 saw swift pullbacks of 5–7%. Conversely, when positive news emerged (such as delays in tariffs or the promise of high-level negotiations), equities rallied. Investors flocked to safe havens (like U.S. Treasuries, gold, and the Japanese yen) during the escalations, mirroring what we’re seeing now (Tariffs rattle stock markets, but long-term impact is unclear | Invesco US).

Despite those scary headlines in 2018–19, it’s important to remember that the longer-term market impact proved to be limited once the situation stabilized. The trade war did cause real economic disruptions – e.g. slower manufacturing activity, higher prices for some goods, and uncertainty that hurt business investment (Tariffs rattle stock markets, but long-term impact is unclear | Invesco US). U.S. companies reported tariff-related cost increases and supply chain adjustments, and sectors like agriculture suffered from retaliatory tariffs. Yet, by late 2019, the U.S. and China reached a preliminary “Phase One” trade deal that paused further escalations. With that relief, the stock market recovered strongly. In fact, after a modest –4.4% decline in 2018 amid the trade battles, the S&P 500 surged by over 31% in 2019 once a resolution was in sight. Chinese equities followed a similar pattern: after a steep 30% drop in 2018, the MSCI China index bounced back over 36% in 2019. In other words, tariff-driven sell-offs were eventually reversed when cooler heads prevailed and policy clarity emerged.

The lesson from 2018–2019 is that markets are highly reactive in the short run – they price in worst-case scenarios quickly – but they can also recover just as fast if actual outcomes turn out less dire. Investors who stayed the course through the trade war volatility were rewarded when markets rebounded (Tariffs rattle stock markets, but long-term impact is unclear | Invesco US). Those who panicked and sold at the depths of the scare would have missed one of the best years for stocks in recent memory (2019). It’s a powerful reminder that while trade conflicts can spur corrections, they have not permanently derailed the market’s longer-term upward trend in the past.

None of this is to minimize the current risks. Today’s tariffs are arguably broader than those in 2018, and uncertainty remains high. But historical context – from the extreme case of Smoot-Hawley to the more recent U.S.-China spat – suggests that knee-jerk sell-offs are often followed by recoveries once initial fears give way to a clearer assessment of the actual economic impact. As investors, understanding these past episodes can help frame our expectations: tariffs tend to be a headwind, but not an insurmountable one. Policymakers also learn from history; already, there are hints of potential negotiations or carve-outs that could mitigate the damage if the global response to these tariffs is too severe.

Long-Term Investors: Keep Calm and Stay the Course

It’s natural to feel anxiety when markets swing wildly on news like this. However, it’s crucial to maintain a long-term perspective. History has shown that short-term market shocks – whether trade wars, geopolitical events, or even pandemics – tend to be temporary. The global economy and markets have proven resilient over time. While volatility is elevated right now, the fundamental picture (interest rates, corporate earnings, consumer demand) hasn’t drastically changed overnight. As long-term investors, we should remind ourselves that pullbacks are normal on the path to longer-term growth. In fact, the S&P 500 experiences an average intra-year decline of about 14% even in normal years, and a 5–10% correction is not unusual multiple times per year. Despite these regular dips, the market’s overall trajectory has historically been upward, with the S&P 500 delivering strong positive returns over time.

Periods of uncertainty – like this tariff turmoil – can actually be healthy for markets, prompting excesses to be trimmed and setting the stage for the next advance. It’s worth noting that before this pullback, equities had rallied strongly for the past two years. A breather, while uncomfortable, is not wholly unexpected. Long-term investors who stick to their plan have generally been rewarded for their patience. As the saying goes, “Time in the market beats timing the market.” Trying to jump in and out to avoid short-term losses often results in missing the best recovery days. For instance, many investors who fled stocks during the worst of the 2018 tariff news missed the swift rebound in 2019. Similarly, those who sold in panic during the March 2020 COVID crash likely missed the remarkable rally that followed.

Staying invested through volatility does not mean ignoring risks; it means acknowledging that volatility is the price of admission for long-term growth in equities. Over the past century, the U.S. stock market has weathered world wars, recessions, oil shocks, and yes, trade wars – yet it has continued to climb over the decades. The current tariff showdown is another test, but not an unprecedented one. It’s important to avoid making emotionally driven portfolio changes in response to headlines. Pullbacks can even present opportunities – for example, to rebalance or add to positions in quality investments at lower prices, if appropriate for your plan. As always, ensure your portfolio is aligned with your risk tolerance and goals. If the volatility is making you lose sleep, talk to your advisor about potential adjustments – before selling everything in fear. Often, a well-diversified portfolio is already built to handle these bumps.

The Value of Diversification Shines

Diversification – spreading investments across different asset classes and geographies – is proving its worth in this environment. When one segment of the market zigs, another often zags. While U.S. large-cap stocks have been hit hard by the tariff news, other areas have held up better (or even gained), cushioning portfolios that are broadly diversified. For example, international stocks have shown resilience: earlier this year, European equities delivered their best start in decades, with double-digit gains through February. Even now, some markets overseas are weathering the storm relatively well. Emerging-market stocks, which lagged in recent years, were actually up year-to-date through Q1 as U.S. markets declined. This means investors with globally diversified equity exposure may have seen smaller overall losses than those concentrated solely in U.S. stocks.

Diversification across asset classes is also key. High-quality bonds are acting as shock absorbers, as we saw with the rally in U.S. Treasuries. Many balanced portfolios have benefitted from their bond allocations rising in value, offsetting some stock declines. In fact, core bonds (as measured by the Bloomberg U.S. Aggregate index) are up roughly 2% so far this year, even as equities have fallen. Holding bonds and other defensive assets provides stability and liquidity – crucial for riding out equity downturns. Gold, too, despite a small pullback yesterady, remains near historic highs and can serve as a hedge if trade tensions persist.

Likewise, within equities, diversification among sectors and regions helps. The tariffs have very different impacts on different industries. U.S. technology and consumer discretionary stocks, which rely heavily on global supply chains, have dropped the most. But more domestically oriented sectors (utilities, real estate, etc.) or tariff “immune” areas have relatively outperformed. Even within the U.S., small-cap stocks are down ~4–5%, similar to large caps, but many small-caps have less direct foreign exposure, which could help if trade frictions continue. Internationally, some economies might even find opportunities: for instance, if Chinese goods become pricier in the U.S., countries like Mexico or Vietnam could fill the gap for certain exports (benefiting their industries). A globally diversified investor can potentially capture gains in those areas to offset losses elsewhere.

The main point is that a well-diversified portfolio is designed to withstand shocks and participate in recoveries wherever they occur. No one can predict with certainty which asset class or region will outperform in a given year. By diversifying, you increase the odds that you’ll always have some winners to balance out the losers. The recent volatility has reinforced this truth: year-to-date, international stocks and bonds have helped soften the blow of U.S. market declines, underscoring why we preach global diversification as part of a sound strategy.

Real Economy Impact: Businesses and Consumers in the Crossfire

Beyond the flashing red numbers on trading screens, what do these tariffs mean for businesses and consumers? In short, significant disruption. Many U.S. companies are scrambling to assess how the tariffs will hit their costs and supply chains. The immediate stock price moves tell a story about anticipated impacts: for example, shares of Nike, an iconic U.S. retailer that manufactures a huge share of its apparel and footwear overseas, plunged 11% on Thursday. Investors anticipate that tariffs will drive up Nike’s cost of goods (since items made in Vietnam, China, etc. will incur new duties) and/or force the company to raise prices, potentially hurting consumer demand. Likewise, Apple’s stock fell around 7–8% as the tariffs threaten to disrupt its China-dependent supply chain and raise the cost of iPhones and electronics. Chipmakers like Nvidia and TSMC also dropped, given their reliance on cross-border tech components. These market reactions suggest that companies with deep global supply chains are expected to feel the most pain – either absorbing higher costs (squeezing profit margins) or passing them to consumers (risking lower sales).

For American consumers, the tariffs could translate into noticeable price increases on a wide range of products. Tariffs are essentially a tax on imports, and businesses often pass at least a portion of that tax to end buyers. Analysts estimate retail prices on many imported goods could rise by mid-to-high single-digit percentages under the new tariff regime. One UBS analysis, for instance, predicts about a 6% average price hike on luxury goods in the U.S. due to tariffs. Everyday consumer products – clothing, shoes, electronics, home goods – are likely to see price tags creep up if the tariffs remain in place for long. This acts like a pay cut for consumers’ wallets, potentially slowing spending if households become more cautious. However, it’s also possible retailers and manufacturers will try to soften the blow by sourcing from alternative countries not facing extra tariffs, or by accepting lower profit margins (as Treasury officials optimistically suggested, hoping foreign vendors “eat the cost” of the levies). In reality, some mix of cost absorption and price increases will occur, but consumers should be prepared for some inflationary effect from these tariffs.

U.S. businesses are making tough choices right now. Import-dependent manufacturers may have to reconfigure supply lines or even relocate production. We’re already hearing anecdotes: the CEO of one mid-sized U.S. manufacturing firm (Milwaukee-based Husco International) said that a small tariff (5%) could have been managed, but double-digit tariffs completely change the calculus (The Day Trump’s Tariffs Shook Wall Street and Corporate America - WSJ). With the new levies, it might no longer be cost-effective for them to import certain components for assembly in the U.S., so they are considering shifting more production overseas to avoid tariffs. Ironically, that’s the opposite of what the tariffs intended – instead of bringing jobs back, overly steep tariffs could deter domestic production by making imported inputs prohibitively expensive. Other companies, especially in industries like autos and machinery, are warning that they can’t quickly replace foreign suppliers with U.S. ones. Building new factories or finding new local suppliers will take years and significant investment, if it’s even possible In the meantime, many firms face tough choices: raise prices, cut costs (perhaps via layoffs or automation), or accept lower profits. None of these are great for the economic outlook in the short run.

Global trade tensions also invite retaliation, which can hurt U.S. exporters and workers. China has already blasted the U.S. tariffs as “unilateral bullying” and pledged to retaliate in kind (The Day Trump’s Tariffs Shook Wall Street and Corporate America - WSJ). We don’t have specifics yet, but based on the 2018 playbook, China could impose its own tariffs on American products – likely targeting sectors like agriculture, aerospace, and automobiles that are politically sensitive. During the last trade war, U.S. farmers were hit hard when China slapped tariffs on soybeans, pork, and other agricultural goods, causing U.S. exports to plunge. Similar retaliatory moves now could again impact American farmers and exporters, potentially driving up their inventories and reducing income. Other countries on the “bad actor” list may also retaliate or file disputes with the World Trade Organization. Already, the EU has hinted at counter-tariffs on U.S. goods (perhaps targeting iconic American exports like bourbon or motorcycles, as they did in 2018). This tit-for-tat dynamic can broaden the economic fallout beyond the initially targeted imports, affecting companies that export U.S. goods abroad.

In the corporate world, executives are navigating uncertainty. A Wall Street Journal report captured the mood: “Markets tumble and executives scramble to grasp the scope and size of Trump’s trade barriers” (The Day Trump’s Tariffs Shook Wall Street and Corporate America - WSJ). Businesses from retail giants to industrial conglomerates spent the last 24 hours on emergency calls with their finance and supply chain teams. Some large multinationals with diversified production (for example, automakers that build cars in multiple countries) might adjust by ramping up output in non-tariffed locations. Others, like many small and medium manufacturers, have fewer options and may simply have to pay the tariff and hope for a policy reversal sooner than later. A few firms (especially U.S.-focused ones) have openly welcomed the tariffs, seeing them as leveling the playing field. There are reports of certain manufacturers considering moving production back to the U.S. to avoid tariffs – the tariffs are seen as an “incentive” by these firms to re-shore factories, which could be a long-term positive if it materializes. However, even those potentially beneficial shifts could cause short-term pain (higher costs and prices until new capacity is built).

For consumers, the impact will become more visible in coming weeks and months. Retailers will gradually adjust prices as tariffed inventory makes its way to store shelves. The timing (just ahead of summer) means back-to-school shopping season could reflect some of these import taxes. Consumer electronics launching later this year might come with slightly higher price tags than initially expected. If you’re planning big purchases that rely heavily on imports (appliances, a car, etc.), it may be wise to monitor prices or even shop sooner rather than later if you can. That said, not all goods will be equally affected – many retailers had already diversified suppliers after the last trade war, and some might eat a portion of the costs to stay competitive. Bottom line: tariffs do trickle down to everyday life. They have been described as a tax on consumers, and while the exact effect varies, many American families could feel a pinch in their budgets if these policies persist.

Stay Balanced and Informed – We’re Here to Help

The past few days have been a whirlwind of news, and we understand that as an investor it’s easy to feel unsettled. Keeping a level head is most important during times like these. We encourage you to lean on the principles of long-term investing: diversification, patience, and adherence to your personalized financial plan. Markets will likely remain choppy in the near term as they digest the evolving trade developments – we could see further swings as additional details (or potential negotiations) emerge. Remember that volatility is not unprecedented and not inherently bad; it’s a normal part of market behavior. The U.S. and global economy have navigated shocks like this before. While we can’t predict exactly how this trade saga will unfold, we have confidence in the resilience of well-allocated portfolios and the benefits of staying invested through short-term turmoil.

Please know that the team here at Kings Path is closely monitoring the markets and the portfolios. If you have any concerns about your investment allocations or risk exposure, don’t hesitate to reach out. We’re here as a resource for you – whether it’s answering questions about the market, talking through the potential impact on your financial goals, or simply providing some reassurance during a worrisome news cycle.

In closing, while President Trump’s new tariffs have clearly injected volatility into the markets and economy, this is exactly the sort of challenge we plan for when constructing your portfolio or developing your financial plan. Global diversification, quality assets, and a long-term outlook are our best tools to weather this uncertainty. We will get through this volatility, as we have before. If you find yourself uneasy or have specific questions about how these developments affect your situation, please contact us. We are here to support and guide you through these turbulent times.

Sources:

What Is the Smoot-Hawley Tariff Act? History, Effect, and Reaction

Tariffs rattle stock markets, but long-term impact is unclear | Invesco US

Smoot-Hawley Tariff Act | History, Effects, & Facts | Britannica

The Day Trump’s Tariffs Shook Wall Street and Corporate America - WSJ